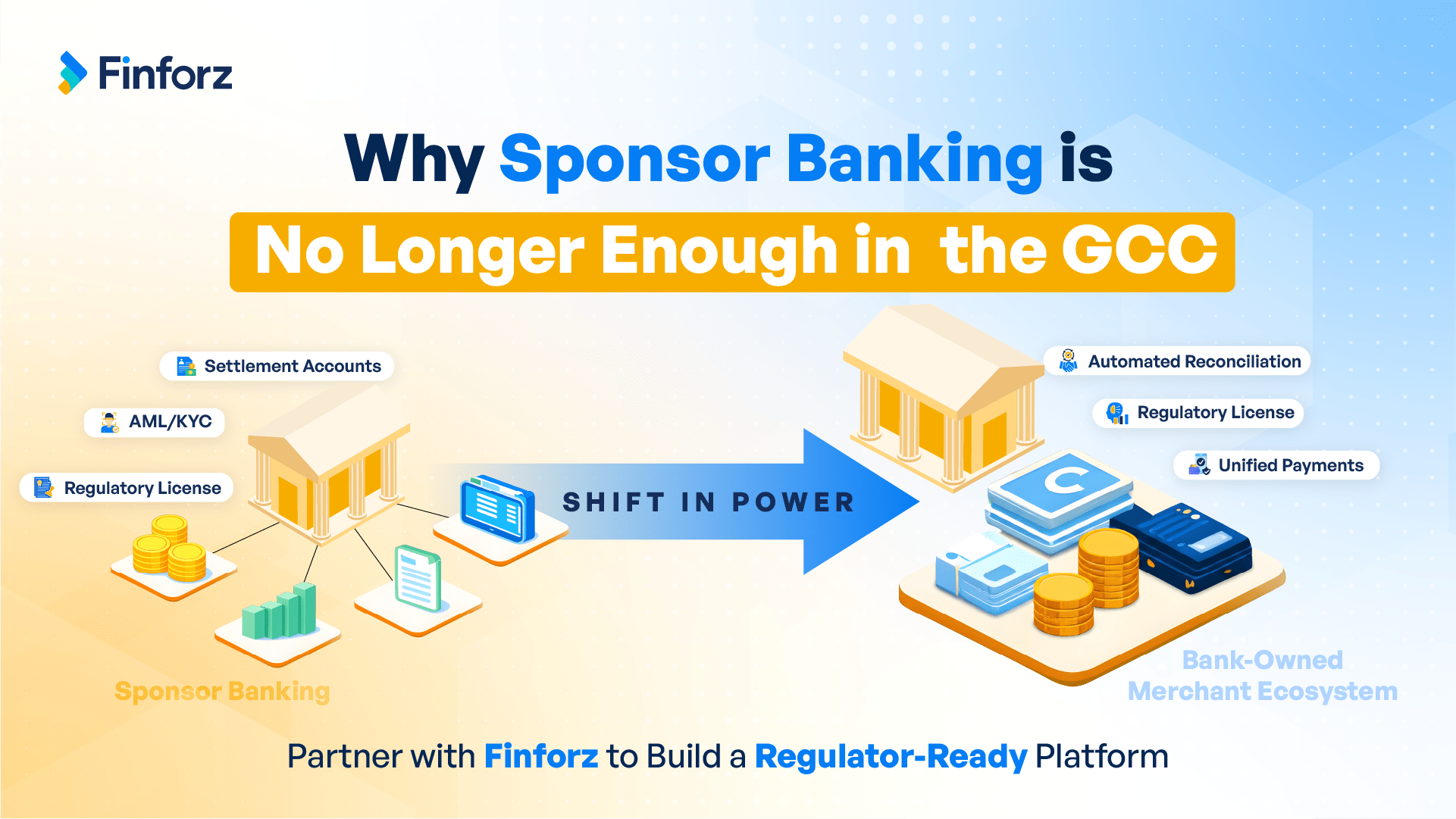

Why Sponsor Banking Is No Longer Enough in the GCC

For more than a decade, sponsor banking has been a practical and effective model across the GCC. Banks provided the regulatory license, settlement infrastructure, and compliance oversight. Fintechs and payment service providers (PSPs) handled merchant acquisition, payments and user experience.

It was a balanced arrangement.

But the market has evolved.

Today, digital payments across UAE, Oman, Saudi Arabia, Qatar, and Bahrain are no longer emerging, they are foundational. Real-time rails are expanding. Wallet adoption is rising. Government collections are digitising. SMEs are moving online. More importantly, SMEs increasingly expect more from their banks. They are not just looking for acceptance solutions, they need better control over collections, recurring billing, cash flow visibility, and reconciliation.

In this environment, sponsor banking is no longer a growth strategy. It is a limiting position.

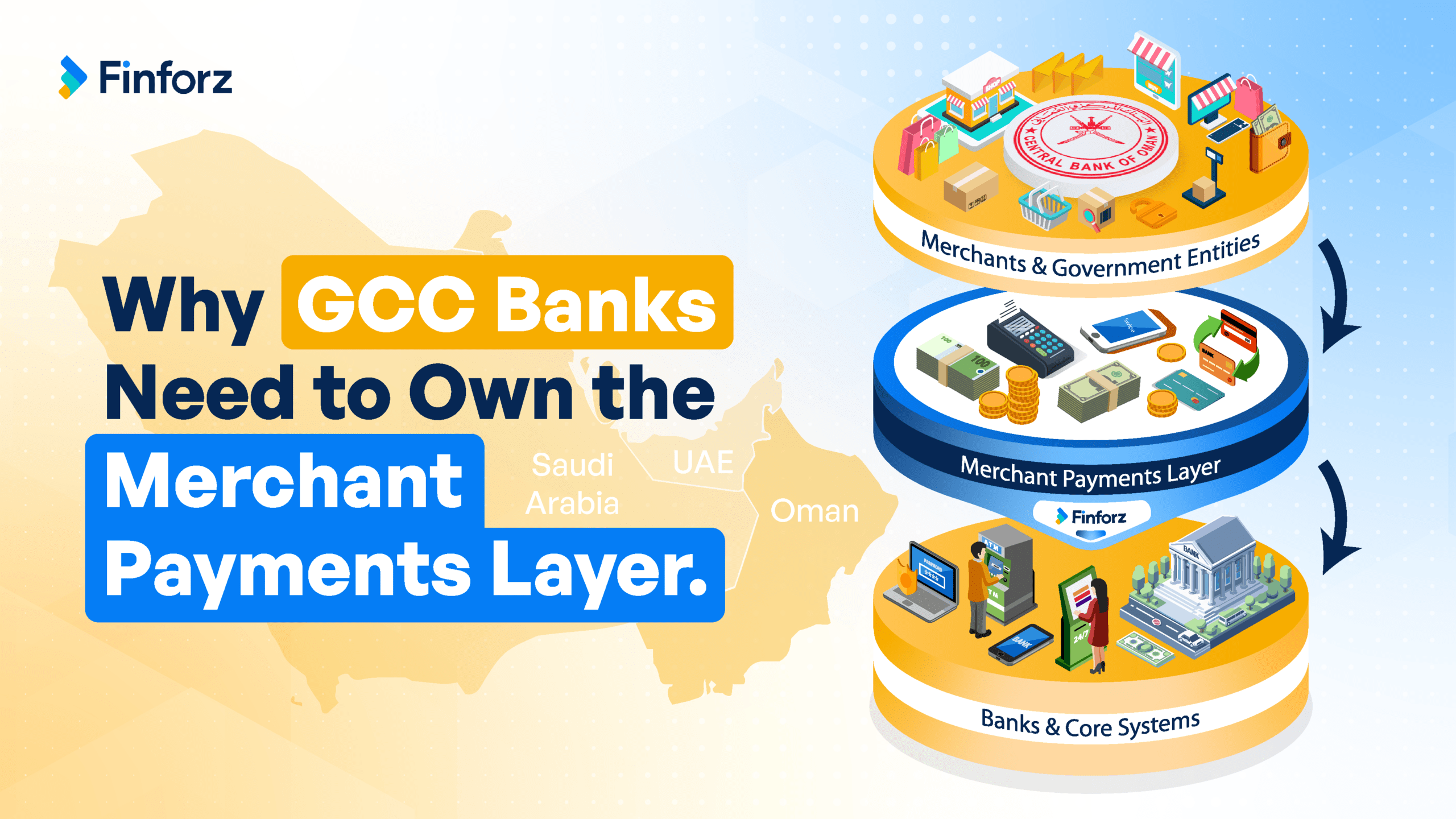

The Shift in Power Within Merchant Payments

Historically, banks sat at the center of financial flows. Today, merchant ecosystems increasingly revolve around platforms.

When banks restrict their role to:

- Settlement accounts

- Regulatory sponsorship

- Scheme access

- AML/KYC validation

They allow others to own:

- Merchant onboarding

- Transaction routing

- Data aggregation

- Revenue intelligence

- Merchant relationships

The result?

Banks carry the regulatory and balance sheet responsibility. Fintechs capture the data, interface, and growth economics.

Across the GCC, where governments are pushing aggressive cashless targets and real-time payment infrastructures this imbalance becomes strategic.

GCC Context: Digital Momentum Is Accelerating

- Saudi Arabia has surpassed ~79% electronic retail payments, driven by Vision 2030 digitalisation goals.

- The UAE continues to expand instant payment infrastructure and wallet ecosystems under strong regulatory frameworks.

- Oman is modernising through OmanNet, MPCSS QR, and ISO 20022 migration initiatives led by the Central Bank of Oman.

- Qatar and Bahrain are strengthening open banking, sandboxes, and PSP licensing frameworks.

Infrastructure is expanding.

Merchant digitisation is accelerating.

Regulation is stabilising.

But the core question for banks is different:

Are we infrastructure providers or ecosystem operators?

The Hidden Cost of Remaining a Sponsor

Remaining in a sponsor-only role creates four structural disadvantages.

1. Revenue Migration

Merchant discount rates (MDR), platform fees, analytics-driven upselling, these move toward the entity that owns the merchant interface.

2. CASA & Float Loss

Settlement balances tied to merchant ecosystems can become powerful liquidity sources. Without ownership of the ecosystem, these balances fragment.

3. Data Blind Spots

Merchant transaction data provides:

- SME credit signals

- Cross-sell insights

- Sectoral risk indicators

- Cash-flow intelligence

Without direct platform orchestration, banks see only partial flows.

4. Compliance Without Control

Regulators demand consolidated audit trails and traceability. Fragmented PSP models often lead to:

- Manual reporting

- Disconnected reconciliation

- Reactive compliance

Sponsor banks carry regulatory accountability without unified operational visibility.

What Modern SMEs Expect From Banks

SMEs and enterprises across GCC markets expect their banks to help them:

- Gain access to a wide network of payment processors and financial institutions through a single platform

- Automate recurring payments and direct debit mandates

- Send timely reminders to improve collection rates

- Offer secure online payment pages and digital e-invoices for a seamless customer experience

- Identify overdue payments automatically and trigger intelligent follow-ups

- Leverage data insights to optimise collections and reduce Days Sales Outstanding (DSO)

These are ecosystem capabilities.

Sponsor banking alone does not deliver them.

The Strategic Transition: From Sponsor to Operator

Leading financial institutions globally have made a key realization:

Owning the merchant payments layer does not mean replacing national rails.

It means orchestrating them.

A modern bank-owned merchant ecosystem enables:

- Unified onboarding & e-KYC

- Multi-rail payment acceptance (QR, gateway, bank transfer, wallet)

- Automated reconciliation

- Centralised reporting

- Compliance-by-design architecture

- Data-driven merchant intelligence

This is where banks regain strategic relevance.

How Finforz Enables Bank-Owned Merchant Ecosystems

Finforz Technologies is purpose-built to help banks in India and the GCC transition from sponsor to operator.

Rather than acting as a standalone PSP, Finforz provides a white-label merchant payment ecosystem platform, designed for regulated environments.

Core Capabilities:

Merchant Onboarding & e-KYC

Structured onboarding aligned to GCC regulatory frameworks, including workflows for Islamic finance review and compliance approvals.

Unified Collections

A single orchestration layer covering:

- QR payments

- Payment links

- Gateway checkout

- Bank transfers

- Domestic instant rails

All under bank branding.

Reconciliation & Settlement Automation

Eliminates Excel-driven reconciliation and fragmented PSP reporting. Provides unified merchant visibility across rails.

Compliance & Audit Trails

Integrated monitoring, reporting modules, and ISO 20022 alignment ensure regulator-ready documentation and transparency.

DataFuze Intelligence Layer

The DataFuze module transforms payment exhaust into actionable insights:

- Merchant performance analytics

- Early risk detection

- Operational monitoring

- Revenue intelligence

This gives banks predictive visibility not just transactional access.

Deployment Designed for GCC Realities

Finforz supports:

- Cloud or hybrid architecture

- Country-specific data residency requirements (including KSA and UAE regulations)

- PCI-DSS compliant integrations

- KYC, AML & sanctions screening integration readiness

- Bank-grade audit logs and dual-control workflows

The platform can be deployed in phases, enabling Tier-2 and Tier-3 banks to participate in the merchant ecosystem without building infrastructure from scratch.

Why This Matters Now

GCC markets are at an inflection point:

- Digital payments are mainstream.

- Government collections are digitising.

- SMEs expect seamless acceptance.

- Regulators demand transparency and real-time accountability.

In this environment, sponsor banking creates structural dependency.

Merchant ecosystems will grow.

The only question is:

Will banks own that growth or observe it?

From Passive Infrastructure to Strategic Leadership

Sponsor banking was sufficient when payments were linear and low-volume.

But in today's real-time, multi-rail, regulator-intensive environment, banks must move from:

Sponsor ➝ Operator

Settlement ➝ Orchestration

Fragmentation ➝ Unified Visibility

Owning the merchant payments layer is not about technology dominance.

It is about strategic control.